Student loans can quietly shape your financial life for years. Whether you just graduated or you’ve been repaying for a while, the right strategy can save you thousands in interest and help you get out of debt faster. Here’s a clear, practical guide to choosing the best repayment approach for your situation.

1. Understand What You Owe

Before choosing a strategy, get a full picture of your loans:

- Total balance

- Interest rates

- Loan types (federal vs. private)

- Repayment terms

Federal loans typically offer more flexibility, especially through programs from the U.S. Department of Education, while private loans depend on your lender.

2. Choose the Right Repayment Plan

Your repayment plan determines how much you pay monthly and over time.

Standard Repayment Plan

- Fixed payments over 10 years

- Higher monthly payments

- Lowest total interest

Best for: Borrowers who can afford higher payments and want to get out of debt quickly.

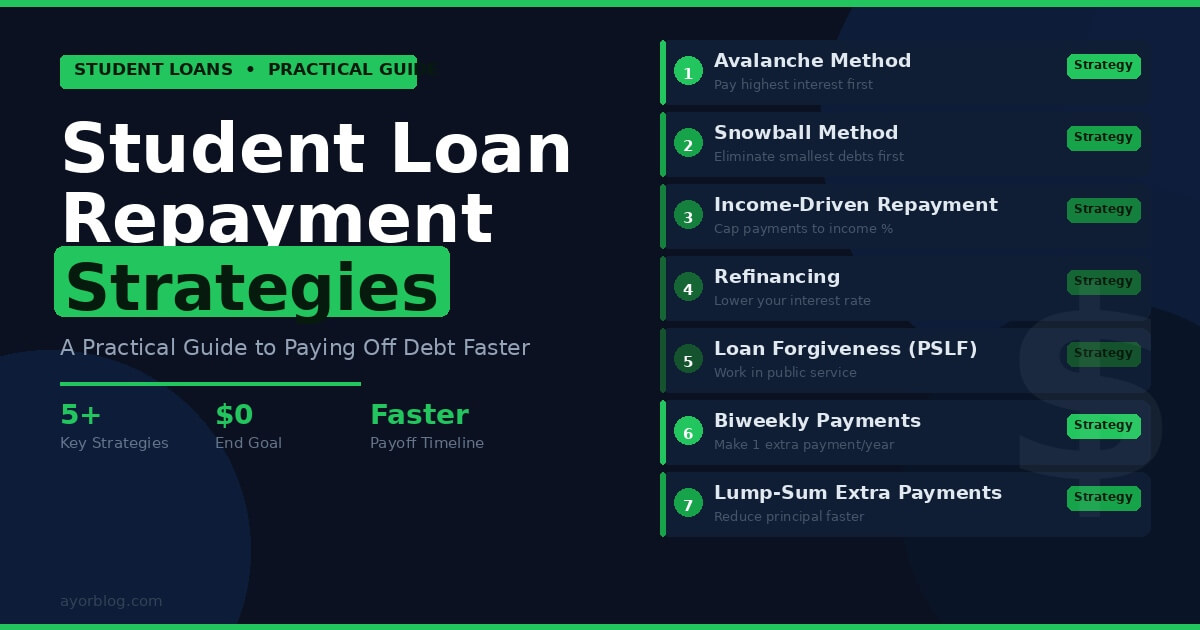

Income-Driven Repayment (IDR) Plans

- Payments based on income and family size

- Loan forgiveness after 20–25 years

Programs like Income-Driven Repayment Plan help make payments manageable if your income is limited.

3. Make Extra Payments When Possible

Paying more than the minimum reduces your principal faster and cuts down interest.

Two popular methods:

- Debt Snowball: Pay off the smallest loan first for quick wins

- Debt Avalanche: Focus on the highest interest loan to save more money

The avalanche method is mathematically better, but the snowball method can keep you motivated.

4. Refinance or Consolidate (With Caution)

Refinancing

Refinancing replaces your existing loan with a new one, often at a lower interest rate. Companies like SoFi and Earnest offer competitive options.

Pros:

- Lower interest rates

- Simplified payments

Cons:

- You lose federal protections (like forgiveness and IDR plans)

Consolidation

Federal loan consolidation combines multiple loans into one, making payments easier but not necessarily cheaper.

5. Take Advantage of Loan Forgiveness Programs

Some borrowers qualify for partial or full loan forgiveness.

Public Service Loan Forgiveness (PSLF)

If you work in government or nonprofit roles, you may qualify for forgiveness after 120 qualifying payments under Public Service Loan Forgiveness.

Teacher Loan Forgiveness

Available for eligible teachers working in low-income schools.

These programs require strict eligibility, so keep detailed records.

6. Automate Payments for Discounts

Many lenders offer a small interest rate reduction (usually 0.25%) for setting up automatic payments. It’s a small win, but over time, it adds up.

7. Cut Costs and Redirect Savings

Look at your monthly expenses:

- Subscriptions

- Dining out

- Lifestyle inflation

Redirect even small savings toward your loans. Consistency matters more than large one-time payments.

8. Build an Emergency Fund First

Before aggressively paying down loans, set aside at least 3–6 months of expenses. This prevents you from relying on credit if unexpected costs arise.

9. Avoid Common Mistakes

- Ignoring interest rates

- Missing payments (hurts credit score)

- Refinancing federal loans without understanding trade-offs

- Only paying the minimum for years

Small missteps can cost you significantly over time.

10. Stay Flexible and Reassess

Your income, goals, and financial situation will change. Review your repayment strategy at least once a year and adjust accordingly.

Final Thoughts

There’s no one-size-fits-all approach to student loan repayment. The best strategy balances affordability, speed, and long-term financial health. Start with a plan you can sustain, then optimize as your income grows.

If you stay consistent and intentional, your student loans don’t have to follow you forever—they can be a chapter you close sooner than you think.